Understanding the Role of Bid Bonds in Construction

A bid bond in construction is a bond that guarantees a contractor will honor its bid if awarded a contract. It involves three parties: the principal (contractor), the obligee (project owner), and the surety (bonding company). Further, bid bonds are commonly required for public construction projects and many large private contracts.

Winning a construction project takes more than submitting the lowest price. Owners also need confidence that the selected contractor will sign the contract and provide the required performance and payment bonds.

That's where a bid bond comes in. It protects project owners from financial losses if the winning bidder backs out or fails to meet post-award obligations.

Whether you're bidding on your first project or expanding your bonding capacity, understanding what a bid bond is, how bid bonds work, and the bid bond requirements can help you navigate the bidding process with confidence. As of 2026, many federal and state agencies continue to require bid bonds, so always review the solicitation documents for the project's specific bonding requirements.

What Is a Bid Bond?

A bid bond is a financial guarantee issued by a surety company. It assures the project owner that the contractor will honor its bid if selected.

If the contractor refuses to sign the contract or cannot provide the required performance bond and payment bond, the surety may compensate the project owner according to the bond terms.

Unlike insurance, a bid bond is a three-party agreement. The contractor ultimately remains responsible for reimbursing the surety if a claim is paid.

Why Are Bid Bonds Required?

Owners use bid bonds in construction to reduce bidding risk. Without one, contractors could submit unrealistically low bids and withdraw without consequences.

Bid bonds help ensure that bidders:

- Submit serious offers.

- Have financial capacity.

- Can obtain final contract bonds.

- Meet project requirements.

- Protect taxpayer funds on public projects.

Public agencies often require a construction bid bond before opening bids. Additionally, large private developers may also require one to reduce procurement risk.

How Do Bid Bonds Work?

While the purpose of a bid bond is straightforward, many contractors are unsure about what happens after the bond is submitted. Understanding how bid bonds work is easier when viewed as a step-by-step process.

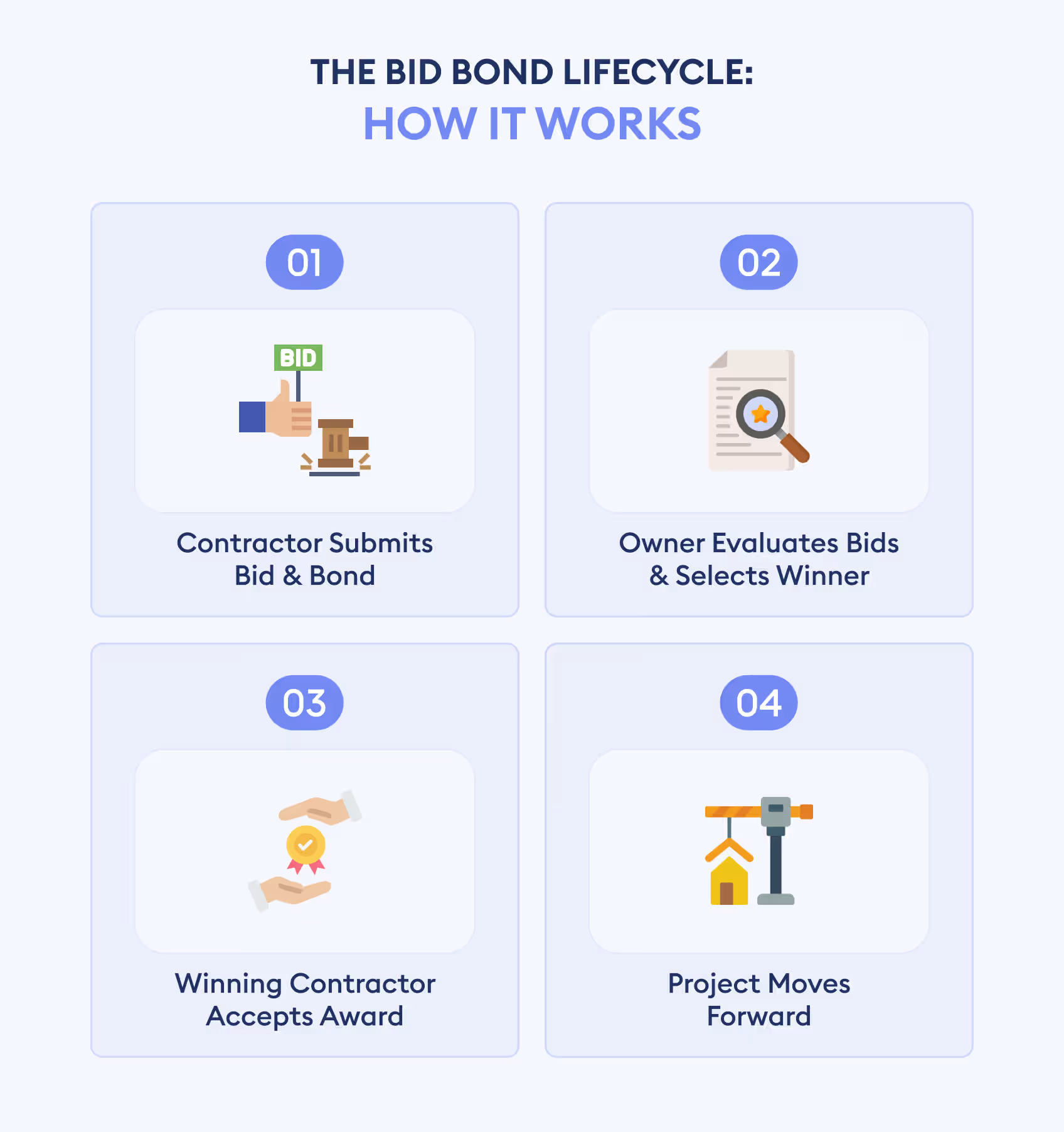

Step 1: Contractor Submits a Bid

The contractor submits a bid along with the required bid bond, which is typically set as a percentage of the total bid value.

Step 2: Owner Evaluates Bids

The project owner then evaluates all qualified bids and selects the contractor offering the best responsive proposal.

Step 3: Contractor Accepts the Award

Once the bid is accepted, the contractor signs the contract and provides the required performance and payment bonds before work begins.

Step 4: Project Moves Forward

Once the contract is executed and all required bonds are in place, it implies that the bid bond has served its purpose, and construction can move forward.

What Happens If a Contractor Backs Out?

However, if the winning contractor refuses to sign the contract or cannot provide the required contract bonds, the owner may file a claim against the bid bond.

The surety company investigates the claim. If valid, the surety compensates the owner according to the bond terms.

The contractor must generally reimburse the surety under the signed indemnity agreement. This process discourages irresponsible bidding and protects project owners from additional procurement costs.

Who Are the Parties to a Bid Bond?

Every construction bid bond involves three legally defined parties.

Principal

The principal is the contractor submitting the bid. By obtaining a bid bond, the principal agrees to honor its bid, sign the contract if selected, and meet all post-award bonding requirements.

Obligee

The obligee is the project owner requesting the bid bond. This is typically a government agency, municipality, school district, or private developer. The obligee is financially protected if the selected contractor fails to move forward with the contract.

Surety

The surety is the bonding company that guarantees the contractor's obligations. Before issuing the bond, the surety conducts surety underwriting to assess the contractor's financial strength, credit history, experience, and available bonding capacity.

Bid Bond Cost

One of the most common questions contractors ask is about bid bond cost.

However, the answer depends on two different figures: the bond amount (penal sum) and the premium. Many contractors confuse the two, but they serve different purposes.

- The bond amount (penal sum): The maximum amount the surety guarantees to the project owner.

- The premium: The fee you pay the surety to issue the bond.

Bond Amount (Penal Sum)

The bond amount, also called the penal sum, is the maximum amount the surety may pay if a valid claim is made. It isn't an upfront cost to the contractor.

Most public agencies require a bid bond equal to 5% to 10% of the total bid value, although some projects specify 15% or even 20%, particularly for certain public works contracts. For example:

The required percentage is always listed in the bid solicitation.

How Much Is the Required Bid Bond Amount?

For most qualified contractors, bid bonds are issued at no additional charge.

Surety companies generally don't earn money from bid bonds. Instead, they expect to issue the performance bond and payment bond if the contractor wins the project, and that's where they collect their premium. In many cases, issuing bid bonds is simply part of maintaining an ongoing bonding relationship.

If a fee is charged, it's usually a small flat administrative fee, especially for one-off requests or contractors without an established surety relationship.

Premium Contractors Pay

On the other hand, premium is the fee paid to obtain the bond. For many qualified contractors, standalone bid bonds have little or no direct cost.

Many sureties include bid bonds at no additional charge when they expect to issue the related performance bond and payment bond if the contractor wins.

If a separate premium applies, it is generally much lower than the cost of performance bonds.

Premiums depend on:

- Credit history

- Financial strength

- Company experience

- Project size

- Bonding relationship

- Surety underwriting results

Contractors with strong financial statements typically receive more favorable terms.

Bid Bond vs Performance Bond vs Payment Bond

Although these contract bonds are often required together, each plays a distinct role in protecting the project

Together, these bonds create a financial safety net throughout the construction lifecycle. The bid bond protects the bidding stage, performance bond protects project completion, and the payment bond helps prevent unpaid subcontractors and potential mechanics' liens.

What Are the Bid Bond Requirements?

Bid bond requirements vary by project owner, and are typically outlined in the bid solicitation. While they're most common on public construction projects, private owners may also require bid bonds for high-value or complex work.

To qualify for a construction bid bond, contractors typically need to demonstrate that they have the financial strength and experience to complete the work if awarded the contract.

Common bid bond requirements include:

- A signed application for a bond

- Company’s financial statements

- Contractor and business license information

- Bid amount and project details

- Borrower’s credit report

- Project relevant experience

- Current WIP reports for larger contractors

- A signed indemnity agreement

For larger projects, the surety may request additional documentation to evaluate the contractor's bonding capacity before issuing the bond.

Note: Many public projects also require the successful bidder to provide a performance bond and payment bond before construction begins.

How to Get a Bid Bond?

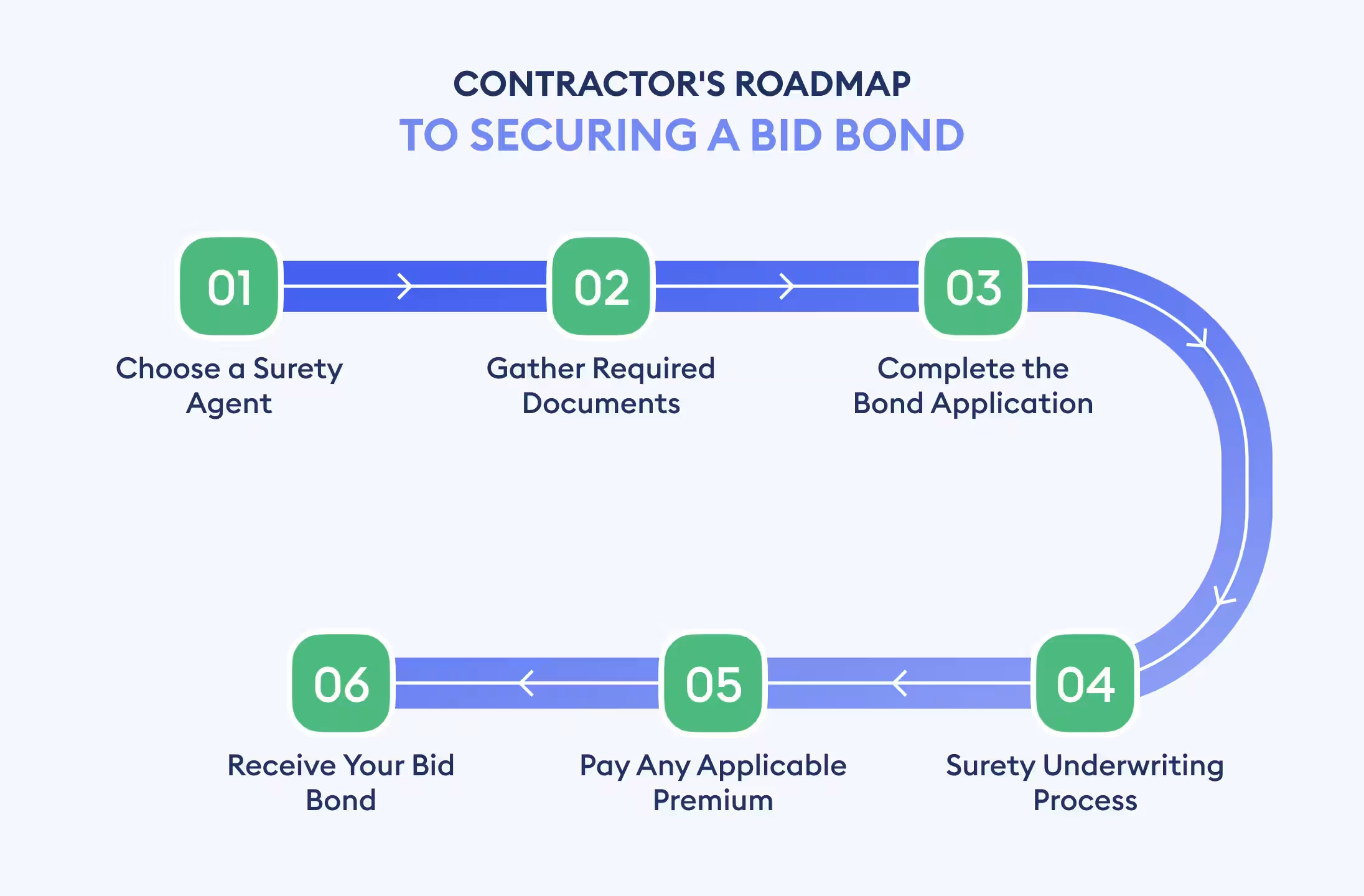

Getting a bid bond is straightforward if you're already working with a surety. While a contractor's requirements vary by surety, most contractors follow these 6 steps before submitting their bid:

Step 1: Choose a Surety Company or Surety Agent

Start by partnering with an experienced surety agency or an established surety company. This type of business will assess your qualifications and guide you to an appropriate bonding solution for your business.

Step 2: Gather the Required Documents

Before issuing a bond, most sureties will require a simple business and a financial statement.

Depending on the project, you may need:

- Financial statements

- Company ownership details

- Project specifications

- Bid amount

- Work-in-progress reports

- Bank references

Step 3: Complete the Bond Application

Finally, submit your application along with the required documents. However, it is important to understand that contractors with an established bonding relationship often complete this step quickly.

Step 4: Surety Underwriting

Your application will then be reviewed by the surety through a process called surety underwriting.

During this review, they assess:

- Financial strength

- Credit history

- Industry experience

- Cash flow

- Existing backlog

- Available bonding capacity

Step 5: Pay Any Applicable Premium

Most qualified contractors receive bid bonds at no additional charge. If a premium or administrative fee applies, you'll need to pay it before the bond is issued.

Step 6: Receive Your Bid Bond

Once approved, the surety issues the bid bond. You can then submit it with your bid before the owner's deadline.

Conclusion

A bid bond is a type of surety bond used in construction contracting. Unlike insurance, which protects the policyholder against covered losses, a surety bond guarantees that a contractor will fulfill its contractual obligations.

Bid bonds are also one of several contract bonds used throughout a construction project. Other common contract bonds include performance bonds, payment bonds and maintenance bonds, each providing financial protection at a different stage of the project lifecycle.

.webp)